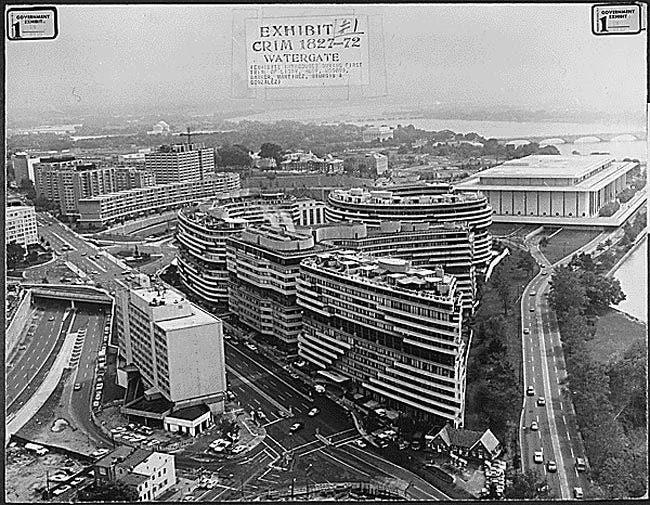

This Day in Legal History: The Watergate Burglary

On this day in 1972, at roughly 2:30 in the morning, a security guard at the Watergate office complex on Virginia Avenue in Washington named Frank Wills noticed that the latches on a stairwell door had been taped over and called the District police. The police arrested five men inside the offices of the Democratic National Committee on the sixth floor: James McCord, Bernard Barker, Virgilio Gonzalez, Eugenio Martinez, and Frank Sturgis. McCord was the security coordinator for the Committee to Re-Elect the President. Two days later, the FBI traced a $25,000 cashier’s check found in Barker’s bank account to the Committee to Re-Elect’s finance chairman. The burglary itself was a third-rate one — bad lockpicking, surveillance gear that did not work, men carrying address books that linked them to the White House — but the legal consequences took two years to play out and rewrote large parts of American constitutional law in the process.

The Senate Select Committee on Presidential Campaign Activities, chaired by Sam Ervin of North Carolina, conducted public hearings in the summer of 1973 that produced the disclosure of the White House taping system. The Saturday Night Massacre in October 1973 — Nixon’s firing of Special Prosecutor Archibald Cox and the resignations of Attorney General Elliot Richardson and Deputy Attorney General William Ruckelshaus — produced the legal scholarship that became the modern law of presidential removal and the Ethics in Government Act of 1978’s independent-counsel framework. United States v. Nixon in July 1974 produced the doctrine that executive privilege is qualified rather than absolute and must yield to a demonstrated need in a criminal proceeding, a holding that is still the foundational separation-of-powers case the Court returns to whenever an administration claims that internal deliberations cannot be subpoenaed.

The articles of impeachment voted by the House Judiciary Committee in late July 1974 produced the modern template for impeachment-as-constitutional-remedy that has been deployed four times since. Nixon resigned on August 9, 1974. The constitutional residue of what began with five men and a roll of tape in a Watergate stairwell is in the Federal Election Campaign Act amendments, the Foreign Intelligence Surveillance Act, the Inspector General Act, the Presidential Records Act, the post-Saturday-Night-Massacre statute book that defines what limits an administration faces when it tries to use the criminal-justice system politically. Fifty-four years on, the question of how much of that residue has held up is, as the saying goes, the question.

U.S. District Judge Lynn Adelman of the Eastern District of Wisconsin on Tuesday denied former Milwaukee County Circuit Judge Hannah Dugan’s post-trial motion to vacate her December 2025 conviction for felony obstruction of a federal proceeding. Dugan had been charged after she let Eduardo Flores-Ruiz, who had appeared in her courtroom in April 2025 on a state misdemeanor, and his attorney leave through a side door of her courtroom after Immigration and Customs Enforcement officers had assembled in the public hallway to arrest him on a federal civil immigration warrant. A jury found Dugan guilty of obstruction and acquitted her of the lesser concealing-an-individual count.

Her post-trial motion pressed two principal arguments. The first was that the Fourth Circuit’s recent decision in United States v. Edwards — which addressed the scope of 18 U.S.C. § 1505 obstruction as applied to interference with administrative agency proceedings — applies to ICE warrant service and so the trial court should have given a narrower jury instruction. The second was that her conduct was protected by the doctrine of judicial immunity for acts taken on the bench. Judge Adelman rejected both. On Edwards, the court held that the Fourth Circuit’s reasoning addresses a different statutory provision and a different agency context, and that Dugan’s case is governed by Seventh Circuit precedent on the obstruction statute she was convicted under.

On judicial immunity, the court held that the doctrine is a civil shield against private damages liability and does not bar federal criminal prosecution for affirmative conduct in aid of evading federal law-enforcement officers. Dugan’s team has announced that the case will go to the Seventh Circuit. Sentencing is now back on the calendar. The appellate question that will dominate the briefing is the one Judge Adelman teed up: whether a state judge taking administrative action in the courthouse — guiding a litigant to a back exit — falls inside or outside the federal obstruction statute’s reach when the action is calculated to defeat federal law-enforcement service. That issue has not been squarely decided in the Seventh Circuit. The case is going to be the vehicle.

Ex-Judge Loses Bid To Undo ICE Obstruction Conviction | Law360

A Maryland federal judge on Tuesday denied SCOTUSblog co-founder Thomas C. Goldstein’s post-trial motion for acquittal or, in the alternative, a new trial on the twelve counts on which a jury had convicted him in February — tax evasion, assisting in the preparation of false returns, willful failure to pay over employment taxes, and false statements to mortgage lenders. The case is one of the more striking falls in modern Supreme Court practice. Goldstein had argued for years before the Court and was, for two decades, one of the most visible private SCOTUS practitioners in the country, with SCOTUSblog itself becoming the standard public-facing reference for Supreme Court news.

The criminal case grew out of his recreational high-stakes poker, which prosecutors used to build out a pattern of unreported gambling income, gambling debts paid out of law-firm funds, and gambling losses claimed as business expenses. The post-trial motion principally argued that the trial court’s jury instructions on willfulness improperly conflated the negligence standard with the higher mens rea Cheek v. United States requires in federal tax-evasion prosecutions, and that the court had wrongly excluded evidence going to Goldstein’s claimed reliance on his accountants’ advice. The court rejected both. On the willfulness instruction, the court found the instruction tracked the Fourth Circuit’s pattern instruction on Cheek and made clear to the jury that a good-faith misunderstanding of the law was a defense. On the accountant-reliance evidence, the court held that the offer of proof was insufficient to establish that Goldstein had actually relied on professional advice in the particular omissions the indictment turned on, as opposed to relying on his own judgment. Sentencing is now the next event.

The federal sentencing guidelines on the tax counts alone, with the loss amount the jury found, point to a substantial custodial term. Watch for an appeal that focuses on the willfulness instruction; that is the cleanest reversible-error vehicle in the record.

SCOTUSblog Founder Goldstein Denied Acquittal Or Retrial | Law360

A Delaware federal judge on Tuesday denied Guardant Health’s post-trial motion to vacate, reduce, or stay enforcement of the $83.4 million jury verdict TwinStrand Biosciences won against it in late 2023 for willful infringement of diagnostic-sequencing patents covering duplex-sequencing technology used in liquid-biopsy cancer-screening assays. The court also declined to enhance the award under 35 U.S.C. § 284, even though the jury had found willfulness, reasoning that the multi-factor Read v. Portec analysis the Federal Circuit has refined in Halo Electronics and its progeny cut both ways here: Guardant’s pre-suit notice and continued use of the accused technology supported some enhancement, but its defenses on infringement and validity, while ultimately rejected, were not objectively reckless.

The decision is notable for two doctrinal reasons. First, it reflects how district courts are continuing to deploy Halo’s discretion-based framework in the post-pandemic-era diagnostic-patent landscape, where the gap between objectively defensible defenses and reckless infringement is being drawn case by case in a way that is making certworthy issues for the Federal Circuit and, eventually, the Supreme Court. Second, it underscores the $83.4 million is significant but not transformative: the broader competitive question in the diagnostic-sequencing space is whether Guardant can design around the asserted claims fast enough to keep its cancer-screening assays on the market without paying a recurring royalty to TwinStrand. Guardant has indicated it will appeal to the Federal Circuit. Both the underlying infringement findings and the no-enhancement ruling are likely to be appealed in parallel — Guardant on infringement and validity, TwinStrand on the refusal to enhance. The verdict stands for now.

Del. Judge Upholds $83.4M Patent Verdict Against Guardant | Law360

My Bloomberg Tax column this week argues that the IRS’s disclosure of taxpayer address information to ICE should be understood less as a narrow immigration-enforcement controversy and more as a tax-data governance failure.

I argue that Section 6103 does not make IRS data impossible to share, but it does make confidentiality the default and disclosure the exception. That distinction matters because a statutory exception should not become a bulk-transfer mechanism whenever another agency wants access to IRS records. The IRS holds unusually sensitive information because taxpayers are legally compelled to provide it, so any interagency disclosure should require necessity, precision, security, and auditability on a record-by-record basis.

The TIGTA report is troubling because the IRS apparently built an automated matching process that was vulnerable to bad ICE inputs, inconsistent formatting, malformed records, and weak matching rules. ICE also had unresolved safeguard issues and missed corrective-action deadlines before the data transfer. In my view, that combination means the problem was not simply that data moved; it was that protected taxpayer information moved through a process that treated matching quality and backend security as implementation details rather than core privacy protections.

The broader point is that bad data inputs are not just a programmer’s inconvenience. If the IRS relies on another agency’s messy file to decide whether protected tax information can be disclosed, the quality of that file becomes part of the taxpayer-confidentiality analysis. Loose input standards and crude matching rules effectively expand the statutory exception beyond what Congress authorized.

My proposed fix is straightforward: before the IRS discloses taxpayer information, requesting agencies should have to provide clean, structured, validated data; legally certify the need for each record; meet defined match-confidence thresholds; submit ambiguous cases for manual review; and accept strict limits on use, retention, and auditing. The column’s central line is that Section 6103 exceptions should operate like locked doors, not loading docks.

IRS Sharing Taxpayer Info With ICE Is a Data Governance Issue